DSCR Loan Rates Hit 4-Week Low While Markets Sleep [Apr/17/2026]

- Eli The DSCR Pro

- Apr 20

- 6 min read

For the week ending on April 17th, 2026

Table of Content

Summary

DSCR loan rates and conventional mortgage rates both dropped 7 basis points this week — with the 30-year fixed settling at 6.32%, the lowest level in about four weeks. The economy isn't collapsing, the Fed didn't cut, and inflation is still running hot. So why did rates quietly improve? Here's the catch: almost nobody noticed — and that silence is exactly the opportunity smart investors have been waiting for.

This week's calm was engineered by a manageable PPI reading that kept bond traders from panicking, combined with a housing market that's slowly thawing. Sellers are returning to the table, inventory is ticking up, and buyers — particularly retail buyers — are hesitating at today's affordability levels. For the methodical real estate investor using a DSCR loan, this combination is rare and genuinely valuable.

By the end of this post, you'll understand exactly what happened in the market this week, how it affects your DSCR loan pricing, and a specific strategy — strengthening your liquidity reserves — that can reduce your rate by up to 25 basis points even when the market barely moves.

The Inflation Data That Didn't Blow Up the Market

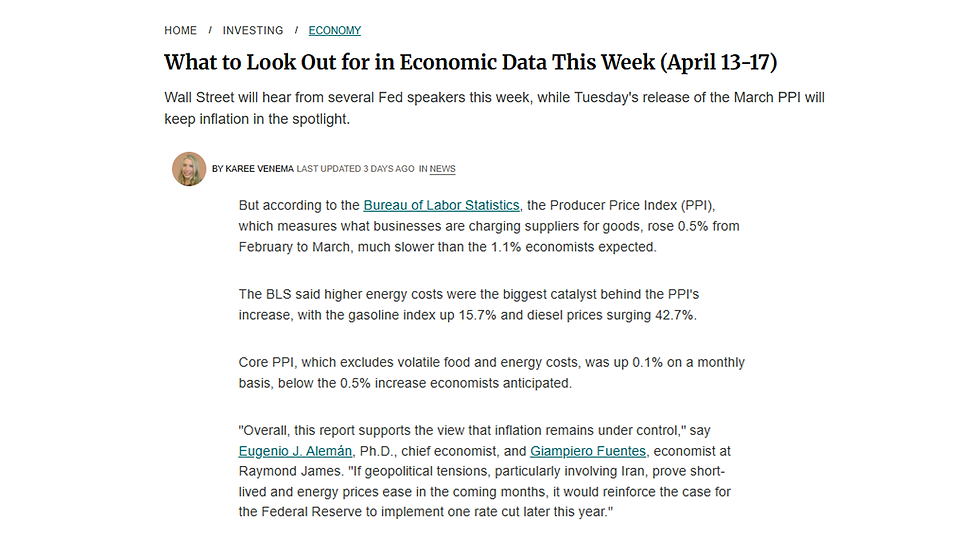

March PPI — the Producer Price Index, which measures wholesale inflation — dropped on Tuesday, April 14th. Markets had been bracing for another inflation grenade after a hot CPI print earlier in the month. Instead, the data came in manageable enough that bond traders essentially shrugged.

The 10-year Treasury yield held its range. Mortgage rates didn't spike. The inflation story that had threatened to push rates back toward 7% simply didn't materialize. That's not headline-grabbing news, but in the current environment, 'no bad news' is genuinely good news.

With bond markets staying calm, DSCR loan rates had no catalyst to climb — and every reason to drift slightly lower into the weekend. The key takeaway: the absence of a negative event can be just as powerful as a positive one when it comes to rate movement.

The Quiet Spring Nobody's Talking About

Beneath the surface of this flat-rate week, something meaningful is shifting. According to spring 2026 housing market data from Redfin and broader inventory tracking, sellers are slowly coming back. After years of inventory being locked up by homeowners unwilling to trade their sub-3% mortgages, listings are starting to tick up.

At the same time, retail buyers are still sitting on the sidelines — cautious about affordability at current rates. That hesitation is creating a window that investors using DSCR loans can step right through. When retail buyers hesitate, days-on-market creep up, negotiating power shifts to the buyer side, and deals can be structured without the panic bidding that defined 2021–2023.

A low-volatility rate environment combined with improving inventory is not a flashy market story. But it's a methodical investor's best friend. You can underwrite with confidence, lock rates without stress, and source deals in a market that isn't on fire — but is finally starting to offer real opportunity again.

Rate Update & Key Economic Indicators

30-Year Fixed Mortgage Rate

Started at 6.39% → Ended at 6.32% | Change: −7 basis points

DSCR Loan Rate (Estimated)

DSCR loan rates currently run approximately 0.75% above conventional, placing this week's DSCR pricing at roughly 7.07% — down slightly from the prior week. On a $400,000 rental property loan, even a 7-basis-point shift changes your monthly payment and your cash flow math in meaningful ways.

Rate Comparison Table:

The labor market softening is actually a net positive for DSCR investors in the long run. Tenants are still broadly employed and paying rent, but the cooling trend gently tilts the macro backdrop in a more rate-friendly direction over the coming months. Neither jobless claims nor ADP signals trouble — they signal a gradual deceleration that favors lower rates ahead.

Lock Now or Wait? Your Move Explained

Here's the honest answer: there is no dramatic catalyst on the near-term calendar that's going to push DSCR loan rates significantly lower in the next few weeks. PPI came in manageable, not great. The Fed is still on hold. And the next major inflation data point could easily push yields back up if it surprises to the upside.

What you have right now is a window — quiet, low-volatility, sitting at a 4-week low — and windows don't stay open forever. If you have a deal that pencils at today's rates, lock it. The math works now. Waiting for another 25 or 50 basis points of improvement while inflation data stays elevated is a gamble, not a strategy.

The investors who win in this environment aren't the ones waiting for perfect rates. They're the ones who structure deals smart enough to work at the rates that exist. That discipline separates investors who consistently build portfolios from those who stay on the sidelines while the market moves without them.

The Liquidity Reserve Strategy That Lowers Your Rate

This strategy is underused and underappreciated by most investors: show strong liquidity reserves.

DSCR lenders don't just evaluate a property's cash flow — they also look at how much cash you have sitting on the sidelines after closing. The logic is straightforward: more reserves reduce the lender's perceived risk. In DSCR pricing, lower perceived risk translates directly into better rates.

We're talking about the difference between a 7.25% rate and a 7.00% rate on some files. On a $350,000 loan, that gap is thousands of dollars over the life of the note. The best part: you don't have to put more money into the deal. You just have to demonstrate that you have it available. Show your bank statements. Show your investment accounts. Show the lender that if anything goes sideways, you can handle it without missing a payment.

This is one of several positioning strategies that can meaningfully improve your DSCR loan terms. If you want to explore which strategies work best for your specific situation — your loan amount, your property type, your reserve position — call or text us directly. Our number is below, and we'll walk you through exactly how to structure your next deal for the best possible pricing.

Ready to Lock Your DSCR Loan at This Week's Rate?

DSCR loan rates are sitting at a 4-week low right now — but these windows close. If you have a deal that pencils at today's pricing, the time to move is now.

📞 Call or text us directly at (718) 300-3503 — we'll review your deal, walk you through your rate options, and help you lock the best possible terms on your next DSCR loan.

We work with investors across New York (Brooklyn, Queens, Bronx, Manhattan), New Jersey, Connecticut, and nationwide on DSCR loans for multifamily (1–20 units), mixed-use, and investment properties of all types — including cash-out refinancing and hard money loan payoffs.

FAQ Section

What are DSCR loan rates today and why did they drop in April 2026?

DSCR loan rates dropped approximately 7 basis points this week, landing at roughly 7.07% for qualified investment properties. The decline mirrors a similar drop in conventional 30-year fixed rates, which settled at 6.32% — a 4-week low. The primary driver was a manageable March PPI reading that prevented bond markets from spiking, allowing mortgage rates to drift slightly lower. For real estate investors in New York, New Jersey, and Connecticut, this represents a meaningful window to lock favorable DSCR financing on 1–20 unit multifamily and mixed-use properties.

Can I get a DSCR loan with Section 8 or CityFHEPS tenants in my rental property?

Yes. DSCR loans qualify properties based on rental income relative to mortgage payment — not the borrower's personal income. Section 8 and CityFHEPS tenants provide government-backed rental vouchers that count as qualifying income in DSCR underwriting. This makes DSCR loans an excellent option for New York City investors with mixed tenant bases, including affordable housing voucher holders. Properties in Brooklyn, Queens, the Bronx, and Manhattan with Section 8 tenants regularly qualify for DSCR financing when the cash flow ratio meets lender requirements.

How do liquidity reserves affect my DSCR loan rate?

Liquidity reserves are one of the most underutilized rate improvement tools available to DSCR borrowers. Lenders assess how much cash you have post-closing as a proxy for risk — higher reserves mean lower perceived risk, which translates directly into pricing advantages. In practical terms, demonstrating strong reserves (typically 6–12 months of PITIA) can reduce your rate by 10–25 basis points depending on your lender and loan file. On a $350,000 investment property loan, that savings can add up to thousands of dollars over the life of the note. You don't need to invest more — you simply need to document what you already have.

Comments